“China views Washington’s competitive measures against Beijing as part of a broader U.S. diplomatic, economic, military, and technological effort to contain its rise, undermine CCP rule, and prevent the PRC from achieving its regional and global power ambitions.“ (p. 7)

What constraints could impede China’s technological and economic march, particularly in high-tech realms? On March 5, 2024, Premier Li Qiang, addressing the National People’s Congress, outlined China’s pivot towards a new development paradigm, earmarking significant investment for technological innovation and advanced manufacturing. This shift, echoing President Xi Jinping’s vision for fostering “new productive forces,” encompasses pivotal sectors like microchip production and defense technology, both heavily reliant on critical resources. In this context, the U.S. strategy appears to pivot towards diminishing reliance on China for these essential materials, concurrently aiming to curb Chinese firms’ ability to broaden their resource bases. As the Caspian Policy Center points out, the escalating Sino-American competition casts the U.S.’s dependency on China for critical minerals as a strategic Achilles’ heel. Dominating nearly 60% of global rare earth mining and over 85% of processing capabilities, China’s potential to leverage its quasi-monopolistic stance in critical minerals poses a significant threat to the U.S.’s high-tech and defense sectors. This was underscored by Beijing’s December 2023 move to restrict exports of certain minerals and related technologies. Yet, some analysts see Central Asian nations as viable contenders in challenging China’s rare-earth metal supremacy.

For China, safeguarding its strategic dominance and thwarting U.S. and allied efforts to tap new critical resource reserves are paramount, especially within the context of global power dynamics. This strategy was underscored following French President Emmanuel Macron’s tour of Kazakhstan and Uzbekistan on November 1-2. Post-visit, Uzbekistan’s Minister of Mines and Geology, Bobir Islamov, revealed a strategic partnership between Uzbekistan and the French firm Orano, with Orano committing to a $500 million investment in uranium extraction and processing in the country. Concurrently, on November 7, Uzbekistan’s Navoiuran and the China National Nuclear Corporation cemented a strategic memorandum for cooperation in the uranium sector, highlighting the intense international competition for critical resources.

In the competition for Central Asia’s critical resources, China and the United States bring distinct strategic advantages to the table:

China:

- Geographic Proximity: Sharing borders with several Central Asian countries, China benefits from easier access and lower transportation costs for extracting resources.

- Financial Resources: China’s substantial financial reserves are directed towards significant mining and infrastructure projects in the region, often as part of its broader foreign policy to foster economic cooperation. This commitment is evident in the considerable funds China and the U.S. have allocated for regional development projects.

- Long-standing Relationships: Through continuous diplomatic and economic engagement, China has cultivated enduring relationships with Central Asian nations, providing a favorable operational climate for its companies.

United States:

- Positioning as an Alternative: The U.S. emphasizes its strengths in innovation, adherence to democratic values, and ethical standards in technology and resource extraction, positioning itself as a counterbalance to China’s influence and offering Central Asian countries an alternative partnership model.

- Global Alliances: The U.S. leverages its extensive network of global alliances and partnerships for resource agreements and investment initiatives in Central Asia. A prime example is the Mineral Security Partnership, aimed at countering Chinese dominance, which includes members like Australia, Canada, Estonia, Finland, France, Germany, India, Italy, Japan, Norway, the Republic of Korea, Sweden, the United Kingdom, the United States, and the European Union. This initiative also reaches out to mineral-rich African nations like South Africa, Botswana, Angola, Mozambique, Namibia, Tanzania, Zambia, Uganda, and the Democratic Republic of Congo, to mitigate Chinese influence.

- Diplomatic Soft Power: The U.S. employs soft power, including educational, cultural, and development assistance, to cultivate relationships that facilitate its strategic objectives in Central Asia, promoting democratic values and responsible corporate practices.

Competition among the great powers for access to critical resources in Central Asia presents a mix of risks and opportunities for the countries of the region. Central Asian countries, with their vast reserves of critical minerals and rare earth metals, can play a key role in the global pursuit of technological progress and energy transition. This scenario unfolds in a broader geopolitical context where these countries are positioned between the interests of major powers such as China, the United States and, to a lesser extent, Russia and the European Union.

Opportunities for Central Asian countries:

- Economic Development and Diversification: The demand for critical resources offers Central Asian countries significant opportunities for economic development and diversification beyond traditional sectors such as agriculture and energy. Investments in mining and processing enterprises can stimulate job creation, infrastructure development and technology transfer, increasing overall economic resilience.

- Strategic Partnerships and Foreign Investment: Growing interest from the U.S., China, and the EU could lead to increased foreign direct investment (FDI) in the region. This influx of capital and expertise can be used to develop other sectors of the economy, improve infrastructure, and build human capital through education and training programs sponsored by foreign partners.

- Improved global standing: By playing a more prominent role in the global supply chain for critical minerals, Central Asian countries can increase their strategic importance on the world stage, giving them greater leverage in international diplomacy and trade negotiations.

Risks for Central Asian countries:

- Dependence on external actors: In their quest to exploit their mineral wealth, Central Asian countries may become overly dependent on one or more external powers for economic stability. Such dependence may limit their foreign policy autonomy and make them vulnerable to economic or political pressure.

- Environmental degradation: The mining and processing of rare earth metals and essential minerals can have significant environmental impacts, including water pollution, soil degradation and habitat destruction. Without strong environmental regulation and oversight, the pursuit of economic gains can lead to long-term environmental damage.

- Socio-economic disparities: The influx of foreign investment and the focus on mining can exacerbate socio-economic inequalities in Central Asian countries. Mineral-rich regions may gain significant development while others lag behind, which may lead to internal tensions and social unrest.

- Geopolitical rivalry: Fierce competition between major powers for access to critical resources can cause geopolitical manipulation in Central Asian countries. For example, some of the resources located on the territory of the countries of the region may be used for military industry, which may not be to the liking of the competing parties.

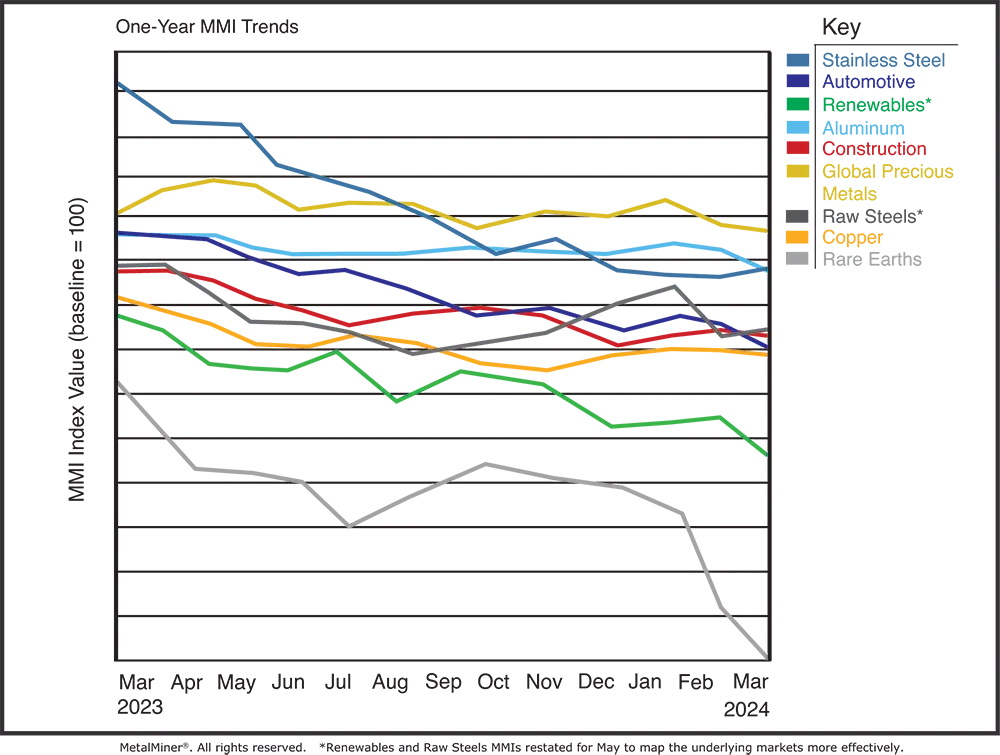

- Price movements in the markets: Rare earth metal prices, as Metal Miner (figure below) notes, have gone down sharply since the beginning of 2024. While weak demand for REM processing (primarily in China, which is a proxy for the country’s stagnant microelectronics industry) may be one reason for the price decline, another potential factor is increased global production and the search for rare earth element reserves outside of China. As Central Asian countries enter the rare earth market, prices for these resources may fall, causing countries in the region to lose some of their potential profits as well.

The place of Central Asian countries in the geopolitics of rare earth metals

Central Asian countries are gradually coming to the forefront of the geopolitical arena related to the extraction and distribution of rare earth metals and are trying to respond accordingly. Thus, the President of Kazakhstan Kassym-Jomart Tokayev in his annual Address to the People of Kazakhstan called for ensuring priority rights to subsoil use to investors who carry out geological exploration at their own expense, adding:

“One of the priority tasks should be the development of deposits of rare and rare-earth metals, which have essentially turned into “new oil”. The countries that will be able to realize their potential in this area will determine the vector of technological progress of the entire world”.

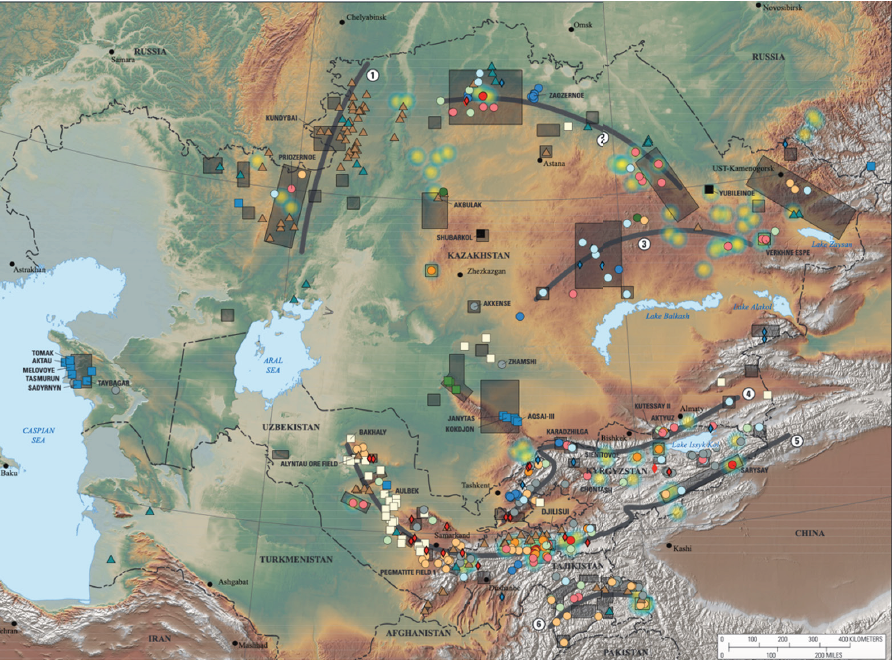

In 2012, the U.S. Geological Survey began assessing the mineral potential of rare earth elements in Central Asia, concluding in 2016 with a list of 384 deposits. This included locations in Kazakhstan (160), Kyrgyzstan (75), Tajikistan (60), Turkmenistan (2) and Uzbekistan (87). The Tien Shan and Pamir regions have also attracted exploration attention given their significant undeveloped resources.

It is currently known that monazite, zircon, apatite, xenotime, pyrochlore, allanite and columbite are among the most common rare metals and minerals in Central Asia. These metals occur in significant quantities, particularly in areas such as the Kazakh steppe, the Tien Shan and Pamir mountains. The potential for mining rare earth elements in Central Asia is significant, which indicates that the development of these resources is promising. Even at this stage, according to a report by the International Energy Agency, the share of minerals and metals in Kyrgyzstan’s total exports is over 50%, while Uzbekistan and Tajikistan have over 30%.

Each of the minerals listed plays a critical role in modern technology and industry, from electronics and energy to aerospace and agriculture, emphasizing the critical importance of rare earth elements and related minerals in advancing technology and supporting global economic development. It was not possible to find exact data on the share of rare earth metals in the world located in Central Asia, but it was not possible to obtain a rough understanding by analyzing data on exports of ores, metals, precious and non-monetary stones. Such data on Central Asian countries is provided by the UN Conference on Trade and Development (UNCTAD).

As Figure 2 shows at this stage, in a generalized form, exports of ores, metals and gemstones are not concentrated on only one of the possible actors, such as China, but are unbalanced between the two major consumers, although Asia's share is gradually increasing. Unfortunately, it is not possible to find more detailed data. As noted by Wesley Hill, head of the international program on energy, growth and security at the International Tax and Investment Center, China does not yet control rare earth mining in Central Asia, despite Chinese activity in the region and China's dominance in mining and processing these resources.

Conclusions

The intensifying competition for critical resources in Central Asia, primarily involving the United States and China, underscores the region's growing strategic importance in the global supply chain for rare earth metals and key minerals. Central Asia's vast reserves of these resources make it a potential counterweight to China's current dominance in the production and processing of rare earth elements needed for high-tech, renewable energy, defense, and automotive industries.

The United States has placed increased emphasis on diversifying sources of critical minerals to reduce dependence on China, as evidenced by initiatives such as the Economic Resilience Initiative for Central Asia (ERICEN) and the C5+1 Critical Minerals Dialogue. These efforts aim to create sustainable and reliable supply chains, promote regional industrial cooperation, and encourage exploration, mining and processing of critical minerals in Central Asia.

On the other hand, China seeks to maintain its strategic position and prevent the U.S. and its allies from accessing new sources of critical resources, as seen in its economic clout in the region and strategic partnerships, such as with Uzbekistan in uranium mining.

Central Asian countries stand at a crossroads, facing both risks and opportunities. They have a chance to utilize their mineral wealth for economic development, attract foreign investment and improve their standing in the world. But they may have to overcome the challenges of geopolitical rivalry, environmental degradation, economic inequality and market instability. The competition between the great powers in the region emphasizes that Central Asian countries need to strategize carefully in order to maximize benefits while mitigating risks, ensuring sustainable development and preserving autonomy over their natural resources.

Main photo: Rare Earth Element and Rare Metal Inventory of Central Asia.