“In just 10 years, China went from a country that did not substantially participate in the financing of the Tajik economy to becoming a major donor. Obviously, there is a simple and comprehensive answer to the question ‘why did it happen?’”- economist Konstantin Bondarenko, writing specially for cabar.asia, states regarding the hidden risks in the nature of Tajikistan’s external debt.

Follow us on LinkedIn!

Tajikistan’s foreign debt is at an approximate total of $2.19 billion and is at least 30% of the GDP while the “threshold” level in the country is set at not more than 40% of the GDP (nominal value). Thus, efforts by the Tajik government to maintain the debt at a sustainable level have for the moment been successful. Regarding the difficult 2009 post-crisis Tajik economy, if the ratio of public debt to GDP was more than 35% in nominal value then this value gradually but steadily declined all subsequent years, reaching 22.5% of GDP in 2014 according to Ministry of Finance data. After 2014, the deterioration of international conditions, which led to slower economic growth and the devaluation of the national currency in Tajikistan, affected the state’s foreign debt. According to available data for April 2016, the ratio increased to 28.2% of GDP.[1]

Tajikistan’s foreign debt is at an approximate total of $2.19 billion and is at least 30% of the GDP while the “threshold” level in the country is set at not more than 40% of the GDP (nominal value). Thus, efforts by the Tajik government to maintain the debt at a sustainable level have for the moment been successful. Regarding the difficult 2009 post-crisis Tajik economy, if the ratio of public debt to GDP was more than 35% in nominal value then this value gradually but steadily declined all subsequent years, reaching 22.5% of GDP in 2014 according to Ministry of Finance data. After 2014, the deterioration of international conditions, which led to slower economic growth and the devaluation of the national currency in Tajikistan, affected the state’s foreign debt. According to available data for April 2016, the ratio increased to 28.2% of GDP.[1]

However, the total foreign debt burden continues to hover at an acceptable level with a public debt management strategy adopted by the government every three years and is executed based on the main indicators. Moreover, some neighboring countries can only dream of Tajikistan’s figures. For example, Kazakhstan’s foreign debt reached 92.3% of GDP or $154 billion by the summer of 2016.[2] Kyrgyzstan’s foreign debt, though not as large in absolute terms, exceeds Tajikistan’s amount by almost half, accounting for about $3.7 billion. At the same time, Kyrgyzstan’s debt came close to 60% of GDP, which is the statutory threshold for the country.[3] Naturally, the following question arises: if the situation with the public debt is stable in Tajikistan, how the can state of the country’s foreign debt point to systemic problems and what are the risks to be covered?

On the hook?

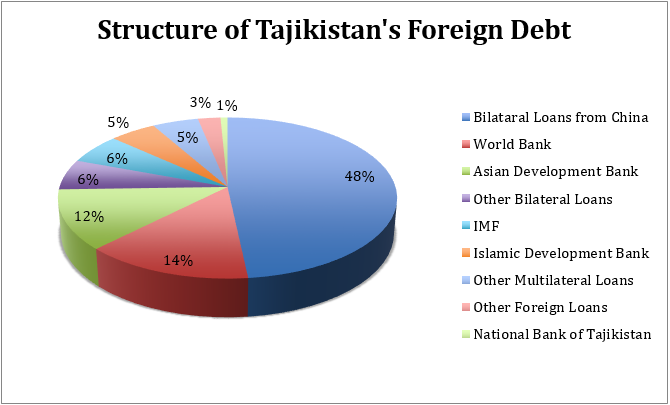

A definite cause for concern may be the noticeable change in the past few years concerning the very structure of the foreign debt along with the emergence in its dominant lender. Today, China has become Tajikistan’s main creditor. Bilateral loans allocated to Tajikistan by China constitute more than one billion dollars, which corresponds to almost half of the total amount of Tajikistan’s foreign debt (48.3% in April 2016).[4]

The proportion of debt for China is absolutely not comparable to the shares of other creditors. The closest “competitors” of China in this regard are the World Bank ($309.6 million with a total debt share of about 14%) and the Asian Development Bank ($263.5 million and a 12% share, respectively). The size of Tajikistan’s foreign debt to China almost reaches the total sum of multilateral loans from international financial institutions.

At the same time, this situation has become a growing issue in recent years. Ten years ago, the amount of debt to China was equal to…zero! For the same period, debt to the World Bank remained steady at $300 million. In just 10 years, China went from a country that did not substantially participate in the financing of the Tajik economy to becoming a major donor. Obviously, there is a simple and comprehensive answer to the question ‘why did it happen?’

Firstly, China’s economic expansion is not directed exclusively towards Tajikistan, but rather to the entire Central Asia region. Neighboring Kyrgyzstan also needed nearly half a billion dollars from its powerful neighbor. China is the main creditor for Kyrgyzstan, but the country has a 38% total volume of foreign debt, which is somewhat lower than Tajikistan’s proportion.[5]

With considerable resources, China has also provided for the development of Kazakhstan’s economy. At the end of 2015, the amount of debt owed to China amounted to $13.6 billion. It is true for Kazakhstan that China is not the only main investor and rounds out the top three after the Netherlands and UK, with a total share in Kazakhstan’s foreign debt of about 9%.[6]

One reason for the strong Chinese dominance of the Tajikistan’s foreign debt is a poor investment climate, which is even more unfavorable than the regional average. Of course, the structure of the foreign debt cannot come from such a conclusion directly. But what else can explain the negligible shares of other countries in the foreign debt? It is also necessary to take into account the fact that the international financial institutions that lend to Tajikistan tend to allocate funds not so much for economic reasons as for humanitarian.

China, with its abundance of resources and general direction of external expansion, can tolerate adverse conditions in recipient countries with credits not being just a necessity but the winning strategy. And if we take into account the nature of preferential lending, China does not actually have to compete with other investor countries, which, of course, will shift the balance of interests in its favor.

As a consequence, Chinese funds allocated to Tajikistan not only have a positive side in the form of concessional conditions but the negative aspect is their so-called “coupling”. Such loans imply that their provision is not only a need to return the principal and interest but also the additional conditions imposed by the lender. Typically, this condition is engaging Chinese companies to implement projects that stand out and are to be allocated funds.

Indeed, the extent of Chinese companies’ presence in Tajikistan can be seen with the naked eye. But in general, this is not something wholly negative. In this case, there is also the creation of jobs and the quality of Chinese construction works, as a rule, is higher than local firms. This may be more difficult for those things that just cannot be seen given that Chinese companies are involved in various sectors. Issues can be, for example, in terms of the control over the use of natural resources, etc.

In addition to considerable financial dependence, a reliance on technology is also growing. After all, in addition to the conditions for the participation of Chinese companies in projects, there is also a need to buy Chinese equipment, which may not always be of the highest quality and also have compatibility issues with equipment from other countries. The list of risks may be greater. In any case, Tajikistan is forming a complex and very strong dependence on China.

Some analysts believe China’s investment activity in Central Asia is a manifestation of so-called “soft power” by its provision of large-scale and affordable financing to be used by Beijing for acquiring the loyalty of other countries and ultimately achieving certain geopolitical objectives.

What does the Tajik government think about it? It is difficult to say, but the lack of capital, especially for the implementation of major infrastructure projects and the cool attitude of other potential investors, does not leave the Tajik authorities wide room for maneuver.

“The Fragile Structure”

If, however, we leave aside the controversial question of China’s fundamental goals via credit extension, there are more tangible problems that arise in Tajikistan’s economy in connection with such intense foreign financing. This is mainly reflected in the artificial stimulation of economic growth, which in this case is concentrated in a small number of industries.

So, as one of the main generators of growth, the construction sector has increased by almost half since 2015 (compared to 43% in 2014), while growth was supported mainly by the implementation of public investment projects worth a total of about four billion somoni. Chinese loans were the main source of funding for these projects. Another growing industry is the mining sector, which is fueled by Chinese investments to a large extent.

Against the backdrop of economic problems and to significantly reduce the level of consumption, the growth of investments in fixed capital, on the contrary, is growing rapidly. At the same time, more than a third of total investments in fixed capital are financed mainly by Chinese loans. All this generates and accumulates a certain disparity in the economy, contributing to the artificial flow of capital between sectors thus making the country as a whole more vulnerable to changes in the international environment.

The World Bank, in its reports on Tajikistan’s economic development, calls this model a “fragile structure at risk” while noting to a certain extent the artificial nature of economic growth and the risks associated with an increase in the amortization of foreign debt.[7]

What if slowing economic growth in China will cause them to dramatically reduce the volume of investments in other countries? Against the backdrop of “shrinkage” of other important sources of external funding such as labor migrants and the virtual absence of domestic sources of growth, this could lead to quite a profound drop in the Tajik economy. Other scenarios are unlikely under the current growth model, which is focused on consumption and public investment and depends on constant foreign support.

Therefore, Tajikistan’s macroeconomic outlook is not as rosy as it may seem from the official statistics on economic growth, including foreign debt. Dependence on external factors, the depletion of foreign exchange reserves, the systemic crisis of the banking sector, and the risks posed by the activities of state-owned enterprises coupled with weak market institutions allow us to speak about the fragile nature of the observed stability.

The government’s task in this situation is a deep restructuring of the economy and carrying out painful but necessary reforms. Significantly reducing in the size of and increasing the transparency of the public sector, reforming the tax code, rejecting direct intervention in the banking sector, and creating favorable conditions for private investment are just a few of their needed goals.

In order to attract foreign funding in this situation, it is better by not “patching holes” in the budget or for promoting extensive growth, but rather for financially supporting reform strategies and mitigating the short-term consequences of their implementation.

References

[1]Ministry of Finance of the Republic of Tajikistan. Accessed October 24, 2016. http://minfin.tj/index.php?do=static&page=gosdolg#vdolg.

[2] Kapital.kz. Внешний долг Казахстана составил $154 млр [Kazakhstan’s foreign debt amounts to $154 billion]. July 20, 2016. https://kapital.kz/finance/52153/vneshnij-dolg-kazahstana-sostavil-154-mlrd.html.

[3] Ministry of Finance of the Kyrgyz Republic. Структура государственного внешнего долга КР по состоянию на 31 августа 2016 [The structure of the public foreign debt of the Kyrgyz Republic as of August 31, 2016]. n.p., 2010. http://www.minfin.kg/ru/novosti/mamlekettik-karyz/tyshky-karyz/struktura-gosudarstvennogo-vneshnego-dolga-kr-po-s3440.html.; Begalieva, Nazgul. “Минфин: Государственный долг Кыргызстана достиг более $4 млрд” [Ministry of Finance: The state debt of Kyrgyzstan has reached more than $ 4 billion]. VecherniI Bishkek (Вечерний Бишкек), September 19, 2016. http://www.vb.kg/doc/347206_minfin:_gosydarstvennyy_dolg_kyrgyzstana_dostig_bolee_4_mlrd.html.

[4] Ministry of Finance of the Republic of Tajikistan.

[5] Ministry of Finance of the Kyrgyz Republic.

[6] World Bank Group. Economic Update No. 1. Spring 2015 ed. n.p., 2015. https://www.worldbank.org/content/dam/Worldbank/Publications/ECA/centralasia/Tajikistan-Economic-Update-Spring-2015-en.pdf; ———. Economic Update No. 2. Fall 2015 ed. n.p., 2015. http://documents.worldbank.org/curated/en/160761467988919181/pdf/101278-REVISED-Box394821B-PUBLIC-TJK-ENG-FOR-WEB-REV.pdf.

[7] Kursiv Research. “Кому должен Казахстан? Рейтинг стран по внешнему долгу” [Should this be Kazakhstan? Ranking countries by foreign debt]. Kursiv.kz, November 24, 2015. http://www.kursiv.kz/news/top_ratings/komu-dolzen-kazahstan-rejting-stran-po-vnesnemu-dolgu/.

Author: Konstantin Bondarenko, economist (Kiev, Ukraine)

The opinions expressed in this article are the author’s own and do not necessarily reflect the view of cabar.asia.