“The hydro-energy complex of Central Asia holds considerable potential, but the uneven distribution of water resources (85 % in Tajikistan and Kyrgyzstan) and the inability of political elites in the respective countries to negotiate, prohibits them both from harnessing it fully, and from solving their energy deficits by alternative means,” writes Sergei Domnin, editor-in-chief of the journal Expert Kazakhstan in an article on regional energy issues written exclusively for cabar.asia

Water, coal and politics

Water, coal and politics

The energy systems of the countries of Central Asia bore little similarities to one another during the time of the Soviet Union and grew further apart in the period following independence. The “Central Asian Ring”, has effectively collapsed and those energy flows that once connected the countries as part of a large sub-regional system are now increasingly insignificant. Currently, Kyrgyzstan and Tajikistan continue to rely on hydroelectric power plants (HEPs), with Kazakhstan and Uzbekistan using more thermal power plants (TPPs). Turkmenistan, in turn is developing gas power stations. Hydropower, while holding significant potential for regional energy cooperation, is unlikely to play any sort of role that reflects this potential in the coming 10-20 years.

Two versus three

The energy relations of the Soviet republics of Central Asia were provided for first by the integrated power system of the USSR, and then by the Unified Energy System of Central Asia (UESCA). The latter is a ring-like network connecting power lines of 220 and 500-kilovolt capacities across a series of power grids in Turkmenistan, Uzbekistan, Tajikistan, Kyrgyzstan and the southern Kazakhstan region [1]. In terms of electricity production for the UESCA, a total of 83 power stations were introduced in the five countries, among which were powerful HEP stations (Nurek in Tajikistan and Toktogul in Kyrgyzstan) and TPP stations (Syrdarya and Novo-Angren in Uzbekistan).

As part of the same system, the the different types of energy production complemented one other. Moreover the water-energy complex was managed from a single center in Uzbekistan. Serving irrigation and energy purposes, the HEPs of Tajikistan and Kyrgyzstan accumulated water in their reservoirs during the winter, cooling production and tapping other resources (coal, gas) from their resource-rich neighbours for their energy needs during the cold months. During the high-snowmelt months of spring and summer, water from the reservoirs was directed to Uzbekistan, Kazakhstan and Turkmenistan for irrigation, and these republics consumed electricity from the HEPs, which by that time was being produced in surplus.

After the Soviet collapse, the problem of energy security became a problem of national security. Each country took the decision to reform its energy system so as to reach full self-sufficiency. Presently, only Turkmenistan, with its relatively low power consumption, has managed to achieve this aim.

Working towards the goal of full energy independence, Kazakhstan increased its North-South energy transit capacity, and forged ahead with plans to strengthen the link between their deficit-laden southern area and surplus-producing North via a North-East-South energy infrastructure backbone. Uzbekistan increased TPP production substantially, but the energy shortages faced by its Andijan, Namangan and Ferghana regions, which traditionally received electricity from Tajikistan, have still not been solved. Turkmenistan built the Seidi-Dashoguz power line, restored Kerki-Voshod and turned its back on Uzbek electricity completely.

Tajikistan and Kyrgyzstan were confronted with the single option of strengthening hydropower capacities, transitioning from systems that stressed irrigation first and power supply second to systems that prioritized power, incurring understandable resistance from the country’s neighbours [2]. This resistance, coupled with a lack of stable funding for their energy projects did not allow the two countries to achieve energy independence and their respective deficits are now covered by their neighbours.

Researchers never tire of pointing out that the hydro-energy complex of Central Asia holds considerable potential (up to 460 billion kWh per year, or almost five times the volume of energy Kazakhstan consumes), but the uneven distribution of water resources (85 % in Tajikistan and Kyrgyzstan) and the inability of political elites in the respective countries to negotiate, prohibits them from both from harnessing it fully, and from solving their energy deficits by alternative means.

Kazakhstan: HEP takes a back seat

The main feature of Kazakhstan’s energy system is its thermal power-generating sector, which is coal and gas-dependent. This sector provides up to 89% of the country’s electrical power production. The HEP sector in turn accounts for about 11% of electricity generation. No more than 0.12% of overall production is provided for by wind and solar power.

TPPs have thus traditionally prevailed in terms of national power generation. This is due to several factors. The first is the relative availability and low cost of coal; up to 54% of Kazakhstan’s total power producing capacities are located in power plants falling within a radius of 500 kilometres from the Ekibastuz coal deposit.

The aggregate capacity of Kazakhstan’s hydroelectric power facilities according to the operator of the national unified power system JSC “KEGOS” amounted to 2584 MW as of 2014. Available capacity drops to 1461 MW in winter, however.

Of Kazakhstan’s existing HEP stations the Leninogorsk cascade (13.8 MW; referring here and subsequently to ‘installed capacity’) launched in 1928 has the longest history. The most modern of the major stations meanwhile is the Moynak HEP, launched in 2011, which reached its current full capacity of 300 MW a year later. In 2013 a series of smaller hydropower stations in Almaty and Zhambyl regions were put into production. The average age of Kazakhstan’s hydropower infrastructure is 36.5 years.

Kazakhstan’s HEP facilities are concentrated in four regions: the East Kazakhstan Region (EKR), Almaty, Zhambyl and South Kazakhstan (SKR) regions. In EKR there is the Shulbinskaya HEP (702 MW) and the Ust-Kamenogorsk HEP (331 MW) in addition to the aforementioned Leninogorsky HEP.

The Almaty region has two stations – Moynak HEP (300 MW) and the Kapchagai HEP (364 MW) as well as the Almaty Cascade HEP (47 MW) and a series of mini-hydropower plants: Aksu -1 HEP (1.9 MW), Issyk HEP – 2 and 3 (6.1 MW), Karatal HEP 2 , 3 , 4 (11.9 MW), Sarkand HEP (0.5 MW), Antonovskaya HEP – 3 (1.6 MW), HEP Uspenovskaya-4 (2.5 MW) and Intalinskaya HEP-5 (0.6 MW).

In Zhambyl region there are the following mini-hydro facilities: Merken HEP- 1, 2 , 3 (3.6 MW), Karakystakskaya HEP (2.1 MW), Tasotkelskaya HEP (9.2 MW). The only HEP in SKR is Shardara. It has an installed capacity of 100 MW that is expected to grow to 126 MW pending completion of an on-going upgrade [3].

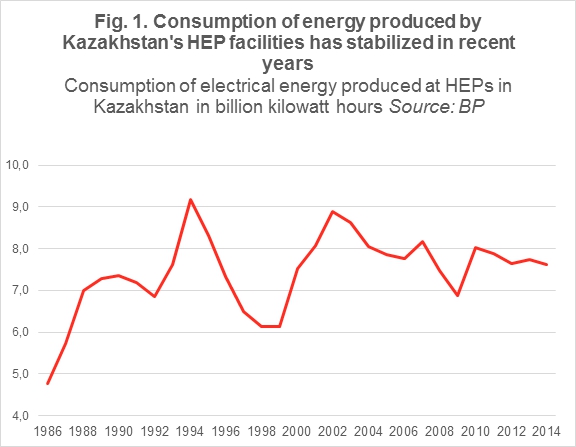

Since all of Kazakhstan’s hydropower stations have a relatively small capacity, their task is to adjust to changing load schedules, performing the classic function of flexible generation while helping to “close out” peaks in consumption. Thus, there is a role for hydropower plants as important elements of a national power system, but their future development remains uncertain. Despite the fact that in the past 25-30 years, the aggregate capacity of Kazakhstan’s HEP sector has grown, the overall consumption of HEP-sourced energy only returned to the levels of the late 1980s by the mid 2010s, according to BP’s 2014 Energy Outlook (see Figure 1).

Central Asia: between necessity and sufficiency

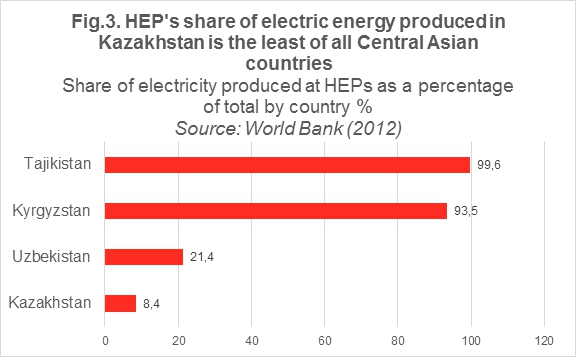

Compared to its neighbours in the Central Asian region Kazakhstan’s hydroelectric power production looks modest. In the ranking of countries in the region in terms of total HEP capacity (see fig.2) Kazakhstan is third, behind Tajikistan and Kyrgyzstan. It is in these countries that HEP enjoys the highest share of total power production (see fig.3).

Tajikistan’s hydropower sector is the largest in Central Asia. According to the International Hydropower Association (2015), the total installed capacity of the local HEP sector is 5190 MW. According to the World Bank (2012), hydropower accounts for 99.6% of total electricity production in the country. In other words, hydropower is the sole and uncontested ruler of Tajikistan’s electricity sector. The largest operating hydroelectric power station is Nurek (3000 MW), with other significant stations in the form of Baipazin HEP (600 MW), Sangtuda-1 HEP (670 MW) from 2008-14 and Sangtuda-2 HEP (220 MW). In addition to these larger hydropower plants Tajikistan operates 300 smaller hydropower plants.

In Kyrgyzstan, hydropower accounts for 93.5% of electricity produced. The total installed capacity of Kyrgyz HEPs according to the International Hydropower Association is an estimated 3091 MW. The largest hydroelectric power stations are Toktogul (1200 MW), Kurpsai (800 MW) and Tash Kumyr (450 MW). The most modern of the country’s power stations is the Kambarata-2 HEP (120 MW), which was launched in 2010.

The combined capacity of hydropower plants in Uzbekistan is 1731 MW and they generate 21.4% of the country’s electricity. Uzbekistan’s hydropower segment today is mainly represented by the 19 HEPs in the Chirchik-Bozsu cascade (Charvak, Hodzhikentskaya, Gazalkent, Tavaksay, Chirchik, Bozsu etc.) with a capacity of 1200 MW. The first link in this cascade – Bozsu HEP – was built in 1926, and the last, Hodzhikentskaya HEP, in 1977.

Turkmenistan has never had notable HEP capacity. The Hindu Kush HEP (capacity 1.2 MW) built in 1913, is the only prominent HEP in the country. There are several mini-HEPs in addition. Due to the high availability of natural gas – Turkmenistan has the world’s fourth largest reserves – gas power plants are in abundance.

The emergence of the ‘mini’ HEP format

The report of the World Energy Council, dated December 2015, notes global electricity generation in the HEP sector is growing both through the development of existing major stations and new mini and micro-hydro stations. This combination increases production without the creation of fresh mega-projects that can fuel public resistance towards hydropower [4].

Some of the countries of Central Asia are moving in this direction. Faced with a prospective shortage of gas within the domestic energy system, the Uzbek authorities see a lot of potential in the modernization of existing hydropower plants and the construction of new, smaller hydropower plants. According to the program of development of hydropower in Uzbekistan 2016-2020 19 HEPs are slated for modernization, “which will allow them to increase their total capacity to 100 MW and in addition generate 450 million kW/h of electricity while saving 200 million cubic meters of gas.” If the projects are implemented, hundreds of small hydropower plants will generate another 1100 MW of capacity [5].

In Kazakhstan, there has not been word of any new big projects since the construction of Moynak HEP, but there are draft plans to build Bulak HEP (80 MW) on the Irtysh river and Kerbulak HEP (50 MW) on the O river. In the last 10 years seven mini HEP projects have been realised. Currently the Ministry of Investment and Development of Kazakhstan is open to investment in 3 HEP facilities: the Useksky HEP (25.6 MW), Chizhinsky HEP (49.6 MW) and Kiyat HEP (1.8 MW) [6].

The impetus for the construction in Kazakhstan of minor energy infrastructure objects, including mini HEPs, has been state support. The vehicles for this support are the provision of soft loans with minimal shared capital required from the borrower and an incentive-based tariff policy that forces grid operators to buy electricity from small hydropower plants, wind power plants, solar power and biogas installations at a fixed rate, indexed annually for a period of 15 years beginning in 2014. Under this scheme, minor HEP facilities sell electricity to the grid for no less than 16.71 tenge per kWh. By way of comparison, Kazakhstan’s largest coal-based TPP – Ekibastuz GRES-1 – sells to the grid at just 8.8 tenge per kWh as of 2016.

We contend that small hydropower facilities are most suited to Kazakhstan’s southern regions, where there are appropriate natural conditions for the construction of such stations.

In Kyrgyzstan, the situation is a little different. The key projects as far as local officials are concerned are the Kambarata-1 HEP (1860 MW) and Upper Naryn cascade HEP (238 MW) projects. Both were initially slated for Russian investment, although the government has since cancelled agreements with two Russian companies amid lengthy construction delays caused by Russia’s economic crisis. Finding new investors for these projects is a priority for the government despite the fact the country could add at least 200 MW of capacity by recovering 39 old HEP facilities and building 87 new mini HEPs). The Kambarata-1 mega dam project meanwhile has met strong resistance from the Uzbek side as it could “lead to a disruption of the water balance in the region”. [7]

Tashkent has raised similar complaints in regards to Tajikistan, which has been trying to build the 3600 MW capacity Rogun HEP for over a decade. The dam would accumulate up to 13.3 cubic kilometers of water from the river Vakhsh, which flows into the Amu Darya river that provides the main irrigation artery for Uzbekistan’s strategic agricultural sector. A World Bank report shows that an operational Rogun HEP would not only increase electricity in the winter, but also contribute to increased production at Nurek HEP (by increasing the power of the turbine). The report’s authors note the project “will be useful and will bring benefits to all the countries of the Amu Darya basin, if they can establish a precise inter-state agreement on optimization of multi-stage use; it will mark a significant improvement in electricity generation, irrigation and environmental objectives.”[8]

However, such a dialogue is inconceivable at present.

Agreements on transit

HEP thus continues to dominate in two of the five Central Asian countries – Tajikistan and Kyrgyzstan – but their respective flagship projects remain in the balance amid political and investment uncertainty.

For as long as Rogun and Kambarata-1 remain politicized, their realization is difficult to foresee. Russia is hesitant to irritate the region’s most populous country Uzbekistan by acting as a partner of the local governments on these projects. Tashkent has also refused to accept the arguments and proposals of its regional partners, and continues to stand its ground. In this situation, it would be more logical for Tajikistan and Kyrgyzstan to focus on projects that do not meet significant political resistance from Uzbekistan.

Examples of such projects include the Upper Naryn cascade. In Tajikistan, there are the successful examples of the Sangtuda HEP 1 and 2: the first station was supported by the Russians and the second by the Iranians. This indicates that the national hydropower segment is still somewhat attractive to investors.

International organizations continue to focus on the potential of small hydro power plants, which the Central Asian countries have largely neglected. But even if this sub-sector grows it may take decades to influence the overall energy picture, and therefore cannot solve the very immediate problem of the winter energy deficits. Resultantly, there should be a complex and comprehensive solution to this problem, the elements of which are already discernible.

In May of this year it is expected that the backbone of a network for transferring surplus power in the summer from Kyrgyzstan and Tajikistan to Afghanistan and Pakistan – CASA-1000 – will be launched. The project is valued at $1 billion and is intended in 2-3 years to promote exports from Central Asia of up to 1300 MW of power.[9]

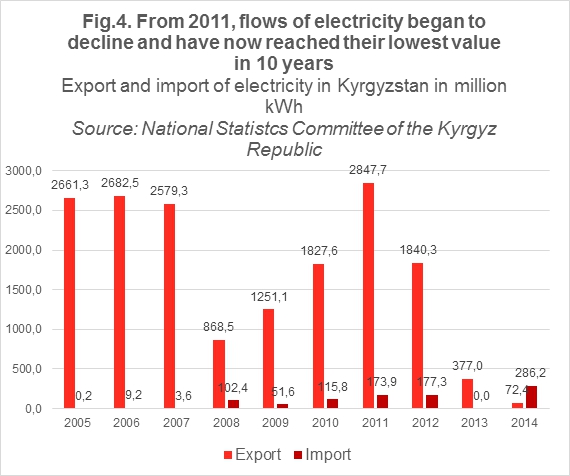

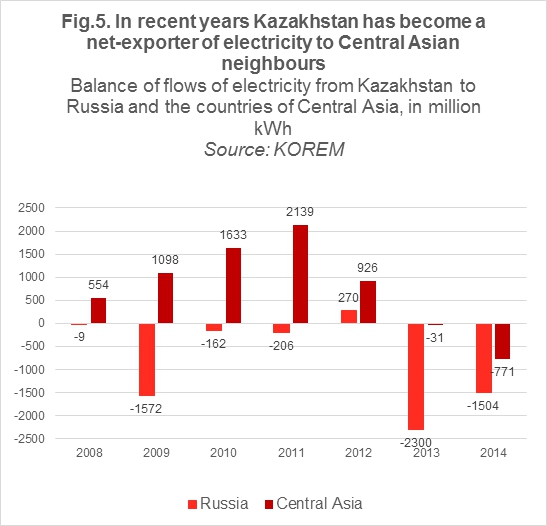

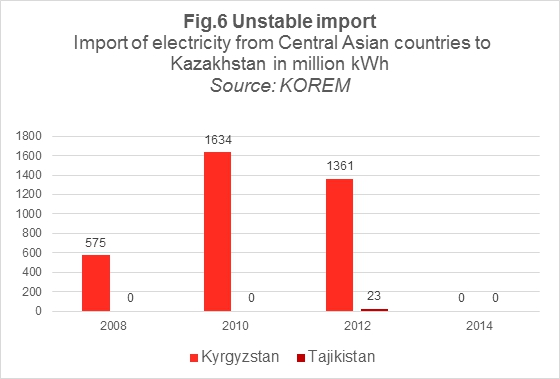

Electricity flows in the last 5-8 years have changed significantly: Kyrgyzstan exports less than ever and imports more and more, while Kazakhstan has reduced imports from Central Asia to a minimum and strengthened its position as a net power exporter (figures 4,5 and 6).

The growing surplus of power emerging in Kazakhstan because of the slowing economy, improved energy efficiency and the reduction of electricity supplies to Russia, can be translated into exports via CASA-1000 infrastructure. Such a scheme might look like this: In winter, Kazakh electricity will be imported by Kyrgyzstan and Tajikistan to cover their deficit. These two countries in turn will transfer their surplus energy to the two South Asian countries — both of whom have growing energy deficits of their own — in summer. At the same time, Kyrgyzstan and Tajikistan will be able to earn a fee for the transit of Kazakh energy. This scheme would buy the export-oriented countries in the region time to iron out internal contradictions.

In conclusion, hydropower, which for the past 50-70 years has been one of the most significant segments of the power industry of Central Asia, has now hit a “political” ceiling. There is still some potential for the development of smaller HEP stations, but at the same time, the region’s countries are all in need of more diversity in terms of sources of energy.

It is irrational to fashion a national grid based on one type of power. That is why Soviet energy planners built a Central Asian energy system combining HEP, thermal power and oil and gas-powered power stations. Renewable energy should not be forgotten either. In Tajikistan alone, solar energy has a potential 24 times as great as that of hydroelectric power. [10]

Sources Used:

- Tomberg, I. Energy of Central Asia: Problems and Potential. Link: http://russiancouncil.ru/inner/?id_4=324#top-content);

- Smirnov, S. Cut it Loose, It Cannot Remain // “Expert Kazakhstan” №46 (237). Link: http://expert.ru/kazakhstan/2009/46/elektroenergetika/;

- Filik, O. Everything is Changing. Link: http://expertonline.kz/a13983/;

- 2015 World Energy Issues Monitor. Link: https://www.worldenergy.org/wp-content/uploads/2015/01/2015-World-Energy-Issues-Monitor.pdf;

- Government Confirms Plan of Program for the Development of Electricity//Sputnik Uzbekistan. Link: http://ru.sputniknews-uz.com/economy/20151007/658327.html;

- List of investment projects of the Ministry of Investment and Development of the Republic of Kazakhstan (data up to April 7, 2016). Link: http://baseinvest.kz/project?generate=1§or_id=22®ion_id=all;

- Atambayev: Uzbekistan is Making a Mistake Opposing the Construction of Kabarata-1//Kloop.kg. Link: http://kloop.kg/blog/2014/11/07/atambaev-uzbekistan-delaet-oshibku-protivyas-stroitelstvu-kambaraty-1/;

- Feasibility Study on the Construction of the Rogun HEP//World Bank. Link: http://www.worldbank.org/content/dam/Worldbank/document/eca/central-asia/TEAS_Reservoir%20operation%20study_Final_rus.pdf;

- Tajikistan, Kyrgyzstan, Afghanistan, Pakistan to launch CASA-1000 in May//KyrTAG. Link: http://kyrtag.kg/society/tadzhikistan-kyrgyzstan-afganistan-pakistan-v-mae-zapustyat-casa-1000;

- Tajikistan: In-depth Review of Energy Efficiency//International Energy Charter. Link: http://www.energycharter.org/fileadmin/DocumentsMedia/IDEER/IDEER-Tajikistan_2013_ru.pdf.

Author: Sergei Domnin, editor of the journal «Expert Kazakhstan» (Kazakhstan, Almaty).

The opinions of the author may not coincide with the position of cabar.asia.