“The dependence of Kazakhstan’s economy on the supply of equipment, software, and services from abroad in developing and maintaining Kazakhstan’s IT infrastructure increases the risk of rising costs in the event of changes in foreign policy and the world economy”, – expert Lesya Karataeva, writing specially for cabar.asia, writes about particular aspects of information security in Kazakhstan.

Traditionally, the concept of security is viewed through the prism of three approaches: the absence of threats, protection, and stability of the system. Obviously, the specifics of the information space make an approach based on an understanding of security absent of threats irrelevant. In particular, based on an interactive map of cyber threats by Kaspersky Lab, Kazakhstan is among the top-30 countries in terms of experiencing cyber attacks, often moving between 18th-27th place.[1] Thus, it makes sense to evaluate information security in the context of relative security and the system’s ability to adequately respond to emerging challenges and threats while minimizing risks.

Traditionally, the concept of security is viewed through the prism of three approaches: the absence of threats, protection, and stability of the system. Obviously, the specifics of the information space make an approach based on an understanding of security absent of threats irrelevant. In particular, based on an interactive map of cyber threats by Kaspersky Lab, Kazakhstan is among the top-30 countries in terms of experiencing cyber attacks, often moving between 18th-27th place.[1] Thus, it makes sense to evaluate information security in the context of relative security and the system’s ability to adequately respond to emerging challenges and threats while minimizing risks.

There is another point that should be noted. Information security is increasingly seen through the prism of the negative consequences of manipulative influences on the minds of information consumers. In assessing cyber security, generally speaking, the discussion goes directly to threats, not challenges and risks, and “under threat” most often refers to the probability of malware. In this paper we propose to look at the existing problems from a different angle. We will examine the environment of implementing some of the objectives of Kazakhstan’s current Information Security Concept, which concludes this year.

According to the concept’s framework, the list of information security threats, as of 2011 (the year of the document’s adoption), includes the following:

- a low level of production while the introduction and use of modern information and communications technology does not meet the objective needs of society;

- a reliance on imports for Kazakhstan’s information technologies and protection of information, which may endanger the country’s national interests.

In order to address the identified threats, the concept seeks to achieve the following goals by 2016:

- develop information technologies and telecommunications;

- increase citizens’ internet access, with 36.6% having access in 2016;

- ensure domestic production of computer equipment, components, associated devices, and software products;

- increase innovation in the industry;

- improve the staffing system in the information security field and protection of state secrets.[2]

What is the current situation?

IT costs

The article presents data for 2015 because 2016 data will be published in February 2017. In 2015, the total cost of IT in Kazakhstan amounted to 375.6004 billion.tenge.[3] In comparison with 2014, the total amount of funding for the IT sector increased by 37% compared to 43% in 2011.

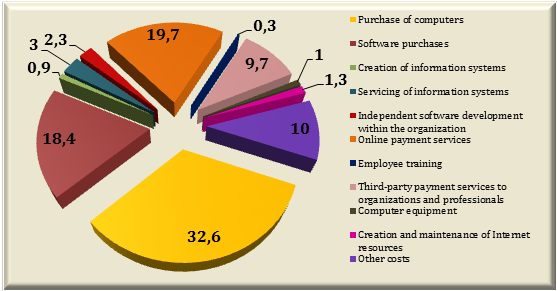

Figure 1. IT sector expenditures in 2015 (% of total costs)

Source: compiled by the author based on the MNE RK Statistics Committee data.

As the diagram shows, the top three IT expenditures are computers (32.6%), online payment services (19.7%), and software purchases (18.4%). This is equally true for both private entities and government agencies. It should be noted that compared with the previous year, the cost of third-party organizations and specialists’ services fell significantly from 20% to 9.7%. The costs to create their own information systems have also fallen and amounted to only 0.9% of the total expenditures. This trend will increase primarily due to state-owned companies, which, as suggested by the new law “On Information”, will gradually transition to the IT service model. State authorities will use such IT-services rather than build their own information systems and acquire the appropriate equipment, etc.[4] It is not essential but does reduce the cost of training specialists (0.3%) and maintaining their own information systems.

Training IT specialists

This is not the first year questions and problems of training Kazakhstani IT specialists have arisen. The differing opinions expressed have not managed to resolve the problem of their own quality-training deficit. Basically, analyzing the situation allows us to speak about its components such as the quality of training in universities, labor market demand, and the willingness of entities to invest in the training and development of their own experts.

Figure 2. Spending on training employees compared to third-party specialist services (% of total costs)

Source: compiled by the author based on the MNE RK Statistics Committee data.

For almost the entire period the cost of third-party organization and specialist’ services showed small but steady growth. Except for 2013, the level of employee training costs remained largely the same. In 2015, the situation was changing and was characterized by a sharp decline in the share of financing to third-party services. At the same time, in absolute terms, finances allocated for training employees decreased by 120%.

In assessing the prevailing situation in the training sector, we should take into account a number of factors. Firstly, the present statistics does not directly factor in the educational sector (universities, etc.) and reflect in-house costs of enterprises and organizations’ employee training programs. Second, digital indicators influence the paradigm shift factor of government institutions in information technology. Third, the concepts of “third-party organization” and “outside experts” does not always mean “foreign”. In particular, the operator of the electronic government information and communication infrastructure service for state agencies is the JSC National Information Technologies. Thus, the decline in performance is not yet cause for alarm.

In the education sector, we can observe an expansion of IT specialist training in higher institutions.[5] At the same time, the question remains concerning the correlation between statistics issued by educational institutions and the number of staff specialists able to create a competitive IT product.

In turn, the lack of advanced practices in “nurturing” Kazakhstani enterprises and companies to develop their own experts is primarily a consequence of the lack of capacity within the domestic IT market while maintaining a relatively low level of application and use of modern information and communication technologies.

Major players of the IT market

Foreign companies deliver a significant amount of services in Kazakhstan’s IT sector. HP, Lenovo, and Acer dominate the PC market. Most of the software market in Kazakhstan is filled with products from Microsoft, SAP, and Oracle. Obviously, Microsoft overshadows its competitors in this area.[6] Russian and Chinese companies, such as Jet Infosystems, NVision, and Huawei, dominate the network integration and consulting sector. Most consulting and software customization services are based on SAP, Oracle, and IBM products.

As for national IT market leaders, their revenues are primarily due to the supply of equipment and software, which is more than 80% of the market. The total cost of software development does not exceed 20%.[7]

Exports and Imports

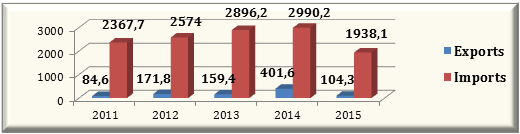

Figure 3. Export and import of IT products (mln. USD)

Source: compiled by the author based on the MNE RK Statistics Committee data.

Official statistics clearly show a sharp decline in 2015 where there was a fourfold decline of exports compared to 2014 and imports suffered heavily as well. The situation can be explained by the IT market’s dependence on Kazakhstan’s macroeconomic performance. At the same time, it fixes the presence of a tangible imbalance between imports and exports in the IT sector. If in 2014 the volume of imports was 7.5 times larger than exports, by 2015 it was 18.5 times more.

In fact, according to statistics, the general trend of technical production in the IT sector up to 2015 has had a positive trend. Annual growth was about 23.5%. However, the IT sector develops unevenly due to varying degrees of output. In particular, the highest growth rates were in communications equipment manufacturing. A small growth dynamic exemplifies the manufacture of electronic components. Consumer electronics production occurs at steady pace without any pronounced growth. Also, there is a sharp decline in the production of computers and associated equipment.[8]

A much more rapidly developing area is e-commerce. The fastest growing segment of e-commerce is travel, which includes services for purchasing tickets and booking hotels, as well as shopping for clothes and home appliances. Also, mobile payment systems, online bill pay, and being able to pay property taxes and fines for traffic violations online are also developing quickly.

The scope of e-government is also growing at an impressive rate.

Internet Access

Such a rapid development of e-commerce and e-government are the result of increased Internet access. According to TNS Web Index data, the Internet is the only growing medium in Kazakhstan, whose coverage is almost two times more than traditional media coverage.[9]

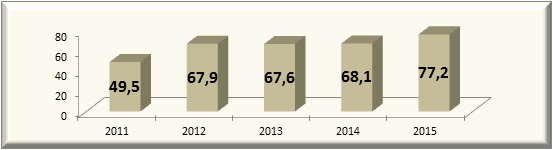

Figure 4. Proportion of Internet users between 6-74 years old (%)

Source: compiled by the author based on the MNE RK Statistics Committee data.

As can be seen from the figures, the current level of Internet users in Kazakhstan is over two times more than that planned in the Information Security Concept. At the same time, one should take into account that the actual level of Internet penetration in Kazakhstan is difficult to determine due to a number of objective factors. First of all you can talk about the differing measurement methods, which are used by different companies. In particular, important metrics such as the age segment and frequency of use are not discussed. Second, quantitative indicators do not reflect the quality of penetration. At the same time, the infrastructure that provides the Internet has seriously evolved. There has been increased speed, reduced access costs, and mobile Internet development. Thus, it should be recognized that efforts to increase Internet penetration have been the most productive in comparison to other metrics.

Conclusion

Thus from the aforementioned data the following conclusions can be drawn.

First, Kazakhstan’s IT industry is focused primarily on the service sector. Second, the dominant mechanism for the creation and development of information technologies in the country is IT outsourcing. This is evident by the assignment of third-party contractors to a range of services (the use or rental of software and so forth) as well as to attract external players to the country in order to develop the IT infrastructure.

Third, issues of import substitution have been neglected. The dependence of Kazakhstan’s economy on the supply of equipment, software, and services from abroad in developing and maintaining Kazakhstan’s IT infrastructure increases the risk of rising costs in the event of changes in foreign policy and the world economy.

Moreover, the use of foreign IT technologies, including in the information security field, potentially increases the risk of leakage in regard to personal user data and loss of control over the information flow altogether. Finally, concentrating on IT outsourcing suggests that public financial resources and resources from private Kazakhstani companies are filling the budgets of the country’s foreign players.

This situation is a consequence of a number of factors, predominantly, an insufficiently large enough domestic market. The low demand for IT technology makes it unprofitable for a company to generate its own IT technologies in-house. In addition, local companies become unprofitable due to the costs of training and maintaining a skilled specialist staff.

References

[1] “Kaspersky Cyberthreat Real-Time Map.” 2016. Accessed October 9, 2016. https://cybermap.kaspersky.com/.

[2] On the Concept of Information Security for the Republic of Kazakhstan until 2016, 2011. http://knb.kz/ru/legal/article.htm?id=10322131@cmsArticle.

[3] The Total Cost of Information and Communication Technologies. Almaty, n.d. Ministry of National Economy of the Republic of Kazakhstan Committee on Statistics. http://stat.gov.kz/faces/wcnav_externalId/homeNumbersInformationSociety?_afrLoop=5538135891477704#%40%3F_afrLoop%3D5538135891477704%26_adf.ctrl-state%3Dl96qjyydy_156.

[4] Zakon.kz. Минус казахстанских IT-производителей – в отсутствии сервис-центров [The downside of Kazakhstani IT-producers’ lack of service centers]. January 29, 2016. http://www.zakon.kz/4771982-minus-kazakhstanskikh-it.html.

[5] Kazakhstan Today. IT-специалистов для Минобороны Казахстана будут обучать в Беларуси [IT Specialists for Kazakhstan’s Ministry of Defense will be trained in Belarus]. July 14, 2016. https://www.kt.kz/rus/education/itspecialistov_dlja_minoboroni_kazahstana_budut_obuchatj_v_belarusi_1153623858.html.

[6] Galiev, Alexander. “Почти 80% всего ИТ-рынка Казахстана – это ‘железо’” [Almost 80% of the IT market in Kazakhstan is “iron”]. Computerworld Kazakhstan, July 14, 2015. http://www.computerworld.kz/articlekz/8899/.

[7] Boitsehovsky, Shamil. “Крупнейшие ИТ-компании Казахстана” [The Largest IT Companies in Kazakhstan]. Computerworld Kazakhstan, June 22, 2015. http://www.computerworld.kz/articlekz/8733/.

[8] Volume of Industrial Products (good. Services) in the ICT Sector (current Prices of Enterprises). Almaty: Ministry of National Economy of the Republic of Kazakhstan Committee on Statistics, n.d. http://www.stat.gov.kz/faces/wcnav_externalId/homeNumbersInformationSociety?_adf.ctrl-state=15nn4sh1da_4&_afrLoop=5547575593187131.

[9] Forbes.kz. Интернет-аудитория Казахстана: портрет и предпочтения пользователя [Internet audience in Kazakhstan: A portrait and user preferences]. June 28, 2015. http://forbes.kz/stats/internet-auditoriya_kazahstana_portret_i_predpochteniya_polzovatelya.

Author: Lesya Karataeva, Ph.D. is Chief Researcher at the Kazakhstan Institute for Strategic Studies under the President of the Republic of Kazakhstan (Kazakhstan, Almaty).

The opinion of the author may not necessarily reflect that of cabar.asia