“Investments are the fastest growing sector of the economy, while the economy itself has been slowing down for the past three years. Notwithstanding world occurrences (i.e. China), the growth of investments in fixed assets by all means should provide an increase in GDP” – expert Sergei Domnin, writing specially for cabar.asia, analyzes the tendencies of Kazakhstan’s economy over the past several years.

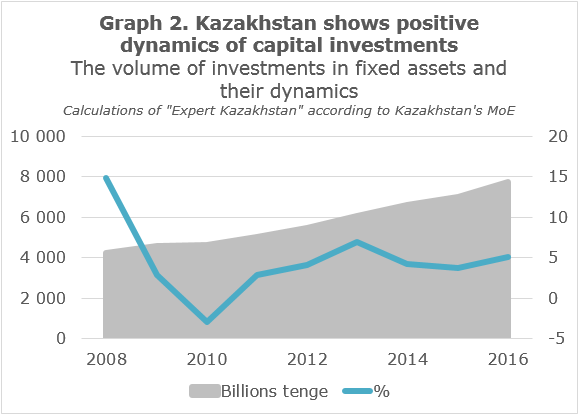

Investments in fixed capital in Kazakhstan by the end of 2016 increased by 5.1%. A higher rate was observed only in a pre-crisis 2008 (14.8%) and the most successful in the last five years was 2013 with 6.9%, respectively. The growth of GDP, according to estimates of the Ministry of National Economy of Kazakhstan (official statistics on GDP have not yet published) is expected to reach 1.0%, the lowest result since 1998.

Investments in fixed capital in Kazakhstan by the end of 2016 increased by 5.1%. A higher rate was observed only in a pre-crisis 2008 (14.8%) and the most successful in the last five years was 2013 with 6.9%, respectively. The growth of GDP, according to estimates of the Ministry of National Economy of Kazakhstan (official statistics on GDP have not yet published) is expected to reach 1.0%, the lowest result since 1998.

In retrospect, for eight years the average economic growth rate was around 4.0%, investment in fixed assets was 4.6%, and in the last four years was 5.0% and 3.1%, respectively. Investments are the fastest growing sector of the economy, while the economy itself has been slowing down for the past three years. Notwithstanding world occurrences (i.e. China), the growth of investments in fixed assets by all means should provide an increase in GDP.

What caused such occurrences in Kazakhstan’s economy these past few years? Is this situation a sign of general inefficiencies in capex (capital expenditures) in the economy? What sectors and regions of the country may overwhelmingly claim the role of investment magnets? How does devaluation of the tenge affect the investment attractiveness of the country? What factors will encourage capital investment in Kazakhstan’s economy? We will try to answer these questions in this article.

Underinvestment or overinvestment?

Investment in fixed assets is defined here as financing the creation of material objects such as new construction, expansion, reconstruction, and modernization of the objects, which leads to an increase in their cost. Capital expenditures may be made both on construction and installation works, the purchasing of machines, equipment, vehicles, and tools, as well as, in the case of agriculture, on husbandry or perennial plantings. Thus, the total amount of investments in fixed assets are included as the money spent on the acquisition of production lines and the construction of factory buildings, wells, mines, ore-dressing facilities, and processing enterprises along with the money allocated towards the construction of houses, schools, and hospitals.

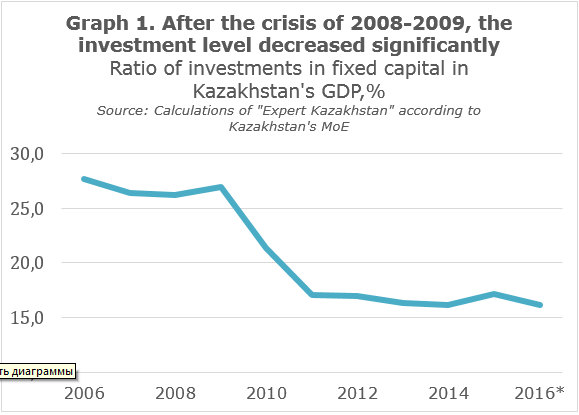

The level of capital investment in this or that economy can be estimated by the ratio of investment to GDP. For the last 10 years in Kazakhstan, the level has altered considerably. In the late 2000s, investments accounted for 26-35% of GDP but dropped to 16-17% after the 2008-09 financial crisis. For comparison, between 2004-08 the world economy averaged 24-25% while China certainly grew (40-43%) and Russia recovered (20-25%). After 2011 and having surpassed Kazakhstan and Russia considerably, Chinese investments added up to 45-47% per annum.

However, the same Chinese example should be observed as a high level of capex transformed into worse economic growth. Between 2004-08, the average GDP growth rate of China was 11.6% but fell to 7.9% from 2011-15. By de facto creating a new economy every two years, China has slowed down. According to most outside observers, it all lies on the inefficient management methods within the Chinese economy.

In recent years, Kazakhstan was faced with a similar situation but at lower rates of GDP growth and investment in fixed assets. On the one hand, investment in the economy is clearly not enough since it has dropped markedly since the mid-2000s. On the other, stable positive dynamics of investment in the last four years have not led to an economic resurgence.

The oil sector, housing, and trade

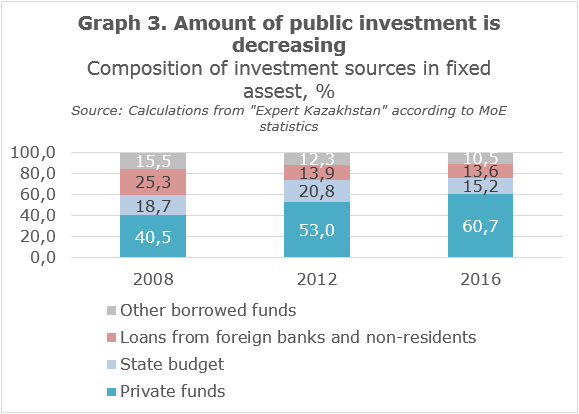

Let us follow the path of fixed assets investments from the sources to the areas of investment. Data provided by official statistics suggests a relatively low share of public investment is directed into the economy. Based on 2016, only 15.2% of capex budgets come from both the national and local levels, while 24.1% is from foreign firms or second-tier banks. The main investors are the traditional owners of the enterprises. However, if their share stood at 40.5% in 2008, then it has increased by half to 60.7% by 2016. This is a good illustration of how the situation in the capital market, with its shortage of long-term, easy loans, and the companies themselves, whose ability to borrow resources for capital projects is affected, are markedly weak.

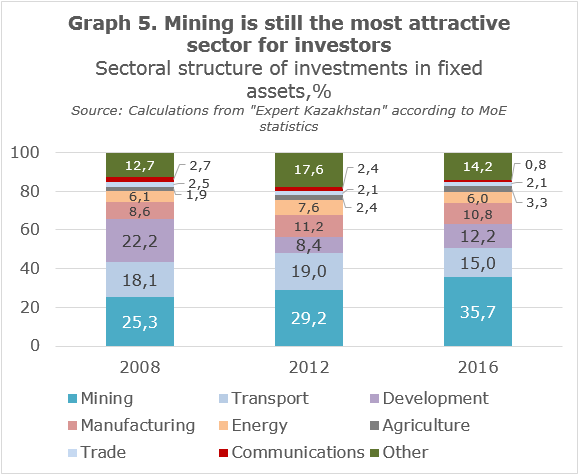

Where capital investment is illuminates the investment structure via attachments. More than two-thirds of investments in Kazakhstan are in three leading sectors: mining, transportation, and real estate development. If you take into consideration the industrial sectors such as manufacturing and energy, the concentration of investments in these five sectors is 80% of the gross volume.

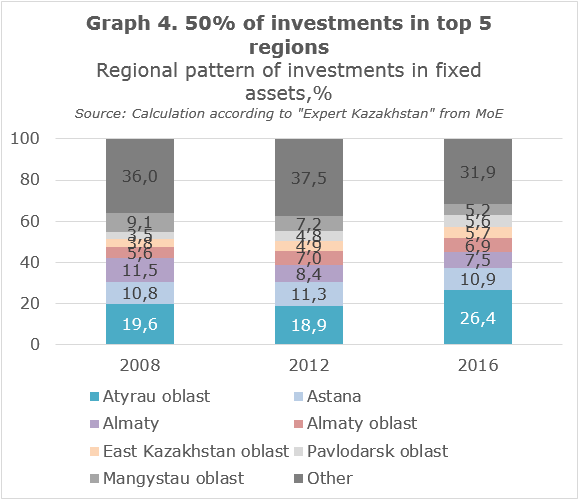

Regional structures of investment allocation do not quite follow the seats of power. Atyrau region is in first place with it being the main oil-producing region of the country but is followed by Astana with its many development projects, large government sector, and a few capital-intensive manufacturing industries. In third place is Almaty, which is the business capital in addition to being home to real estate magnates who facilitate finance and insurance, transportation, and other areas of the service sector. East Kazakhstan and Pavlodar regions, with their large numbers of metallurgical enterprises and power generating centers (coal and hydroelectric), complete the top five regions, which together account for just over 50% of capital investments in the country.

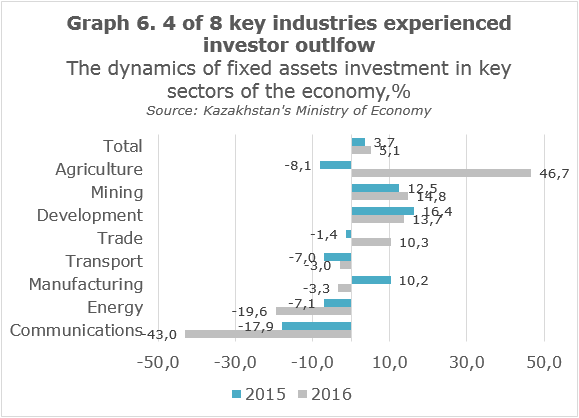

The extraction sector of the country is represented mainly by oil and gas but includes coal, ore, and uranium mining. The demand for these resources both domestically and globally has fallen the past few years. In 2016, capital investments in the mining sector grew by almost 15%. When compared to 2015, the growth rate increased. Investment activity in the sector is related to the implementation of several oil projects, the largest of which are the Tengiz and Kashagan stations.

Also, investments in the real estate sector rose by 13.7% compared to 16.4% a year earlier. The steady flow of funds here is connected with state housing financed by the anti-crisis program “Nurly Zhol”, which has become a magnet for attracting private investment. Impressive growth of investments in agriculture, evenly distributed among crop and livestock production (47.5% and 44.1%), has resulted in high-yield perennial crops, as well as investors’ interest in cattle breeding in Kazakhstan.

There is another factor that could have an impact on investment. Kazakhstani statistics take into account investment in national currency. Foreign investors, such as Chevron and Glencore, and major local companies in all sectors of the economy attract investments in foreign currencies. 49% of deposits of non-banking entities located in Kazakhstani banks are composed of foreign currency. In 2016, the average rate of the tenge to the dollar increased by 54% over the previous year.

However, this weakening of the tenge was caused by a decline in sectoral investments, which were aimed at the domestic market with a high degree of imports in the structure of production costs. An example of this is the manufacturing industry, which started to have problems even during a quite prosperous 2014. While the sector shows close to zero growth in production, some in the industry feel quite comfortable thanks to the improvement of world prices of non-ferrous metals, while others, such as machine building, are in deep crisis. As a result there is a 3.3% volume reduction in capital costs for the whole sector, compared to 10.2% growth in 2015.

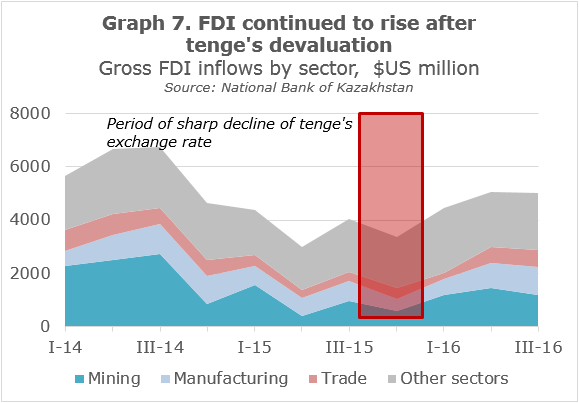

After the tenge’s sudden devaluation, the subsequent stabilization of the exchange rate reassured foreign investors. In the first two quarters following the devaluation, gross inflows of foreign direct investment (FDI) began to grow with the manufacturing industry being the main sector for investment.

The magnet is assembled

In the medium term, the sources and directions of investment patterns are unlikely to undergo major changes. The physical volume of investment in fixed assets will continue to grow, but growth will be the basis for projects in the oil and gas sector. The largest will be the third phase of developing the Tengiz oil and gas field – the Future Growth Project and Wellhead Pressure Management Project (FGP-WPMP). According to the Ministry of Energy, investment in the project, which is slated to be completed by 2022, will amount to about $37 billion. Another project of comparable size would be the third development phase of the Karachaganak oil and gas field, which is projected to cost around $12 billion.

In recent years, the Kazakhstani authorities have taken a number of regulatory measures to encourage investment in the manufacturing sector. In 2014, Kazakhstani legislators drafted provisions allowing customs duty exemptions for investors in priority sectors while providing medium and large-scale projects exemptions from corporate income taxes, land taxes for ten years, and property taxes for eight years. The government is ready to reimburse 30% of the costs for construction and installation work and equipment for the largest “anchor” projects. These measures may help draw foreign magnates while giving them a taste of Kazakhstani projects, which may help macroeconomic endeavors.

In the near future, key events in the real estate sector may be associated only with government incentives. At the end of last year, the Ministry of Economy presented the housing construction program “Nurly Zhol”, in which it plans to send 1.8 trillion tenge of budgetary funds over 10 years, which should generate 16 trillion tenge in private investments. The government subsequently approved the program.

The factors that will stimulate investment in Kazakhstan’s economy in the medium term should include a high potential for subsurface industries, metallurgy, and energy, a favorable regulatory climate, public investment in infrastructure and housing programs, the low cost of land and labor, and proximity to major markets such as China and Russia. However, investors cannot help but take into consideration factors such as high political risk associated with transit authorities in Kazakhstan, the global trend of a declining demand for hydrocarbons and metals, the risk of a further weakening tenge against the backdrop of an ever increasing US Federal Treasury, and increased protectionism from US foreign trade.

Author: Sergey Domnin, chief editor of “Expert Kazakhstan” magazine (Almaty, Kazakhstan).

The opinions expressed in this article are the author’s own and do not necessarily reflect the view of cabar.asia.