“The budget planning system in Kazakhstan leaves much to be desired, with large discrepancies between what is planned and the actual amounts of funding allocated for the Nurly Jol anticrisis program and other measures to support businesses.” – Expert Aidarkhan Kussainov analyzes Kazakhstani budgetary planning and allocations in this cabar.asia exclusive.

The state is one of the largest economic actors in the country as a purchaser of goods and services. If we exclude the market for raw materials, then the state budget is 18% of GDP (if you include geological surveying which is non-budgetary then the share of GDP rises to 35%), because budget expenditures are about 30% of the market for raw materials. In short, government expenditures account for a large share of demand in the economy.

The state is one of the largest economic actors in the country as a purchaser of goods and services. If we exclude the market for raw materials, then the state budget is 18% of GDP (if you include geological surveying which is non-budgetary then the share of GDP rises to 35%), because budget expenditures are about 30% of the market for raw materials. In short, government expenditures account for a large share of demand in the economy.

The behavior of this type of customer, its spending, and its planned purchases in many ways define the sales and investment plans of the raw material private sector. The stability of these plans is key for economic stability, however budget allocations are limited to one financial year. This leads to an ineffective use of state resources, as managers attempt at any cost to implement budgetary programs within one financial year while implementers are absolved of responsibility for the results of a state program or project lasting longer than a year. To solve this inherent contradiction and increase the scope for planning the country moved to three-year budgeting in 2009.

This type of mechanism also elevates the responsibility of implementers for results because this increased budget timeframe allows for a larger degree of maneuvering and flexibility in planning and implementation.

The main problem – adjustments

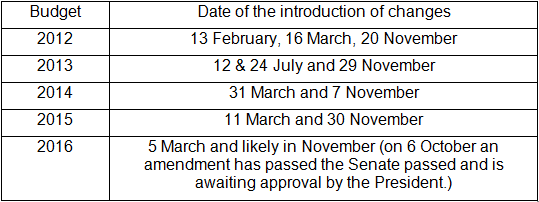

Unfortunately, amending the annual budget over the course of the year has become standard practice in recent years, and these changes have been significant enough to require changes at a legislative level:

Table 1. Number of budgetary amendments, 2012 – 2016

These are only the most serious amendments passed by Parliament and enacted as legislation. There are also a large number of amendments made by the government annually.

The work to pass an amendment through the legislature takes place over the course of a few months. It takes no less than one month to come to an agreement and approve procedures. The number of corrections undertaken within the government also requires time. This means that a significant amount time is spent by the government reviewing and correcting the state budget. The country’s primary financial document, the annual plan, has become a moving target and is losing its meaning. If plans are in a state of constant review, then this means the government is simply reacting to circumstances without a plan and engaged in policy formation.

There is yet another problem. Regular budgetary review reframes actual costs into planned costs, which consequently means it is impossible to judge the quality of planning or figure out which plans have been implemented, which have not, why this has happened, and who is responsible.

For this reason, we are able to identify the following budget amendment periods: the end of the first quarter and the end of the financial year. Introducing changes at the end of the first quarter calls into question the quality of planning and leads to a paralysis in commercial contractual activity. In fact, the procurement process for goods and services and the finalizing contracts are blocked for an entire quarter. Only pre-existing contracts are enacted. The largest consumer of goods and services is simply inactive for the first quarter of the financial year.

Amending the budget at the end of November makes no sense from a policy implementation perspective. These changes have little to no effect on the few remaining months. However, these amendments are perfectly suitable to make projected indicators align with actual indicators. In this case, budget implementation by the end of the year reaches close to 100%, and the “planning” process is recognized only being nothing but accurate and effective.

The true effectiveness of planning

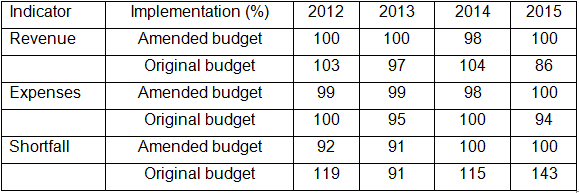

Below is a table of key performance indicators for the budget year. For the purposes of comparison two figures are presented: implementation according to the amended plan (the final November version) and implementation according to the original plan, meaning the budget with which the country began the year.

Table 2. Indicators of Kazakhstani budget implementation, 2012 – 2016

It is apparent that there is considerably more deviation from the original budget plan than from the corrected one, which confirms the thesis that there is an attempt to “align” the budget projections with the facts in November every year.

To understand the significance of this divergence, I would like to point out that the entire Nurly Jol program in 2015 received 686 billion tenge in financing of which 423.4 billion was financed through the state budget. In 2013, there was a decrease of 323 billion tenge in budgetary costs from the original projections. Considering that the global economic situation was quite stable, this is a very significant deviation.

In 2014, the original planned costs were increased by 369 billion tenge in March and then decreased again by 362 billion tenge to their initial level.

In 2015, planned costs were lowered to 404 billion tenge even after taking into account the fact that 423.4 billion tenge to fund the Nurly Jol program was included in budget financing.

Deviations from the planned budget broke all records in 2016. Over the course of only 9 months in 2016, revenues exceeded the plan by 26%. It is curious that revenue projections were decreased by 8% from the original plan during a March 2016 review, but by October the actual revenues exceeded 26%.

Based on this, it appears that the budget planning system in Kazakhstan leaves much to be desired, with large discrepancies between what is planned and the actual amounts of funding allocated for the Nurly Jol anticrisis program and other measures to support businesses. This ineffectiveness is hidden by the constant budget correction procedures, which creates an illusion of precision in the planning and management of budgetary funds.

In conditions of crisis and turbulence, economic uncertainty grows. Prospects for business and society grow dim, and risks grow. Government spending and the budget grow exponentially more uncertain, which exacerbates the problems in the economy. Stability and the predictability in budgetary expenses are incredibly important under these circumstances.

The accuracy of government planning and projections as well as a balanced budget are today of secondary importance. The predictability of government spending is much more important. If state procurement has already been approved, then business could rely on at least this aspect of demand and sales. Currently, the Kazakhstani Ministry of the National Economy (MNE) is prepared to engage in a process of a continual budget review, which means creating a constant level of unnecessary uncertainty.

Procyclicality of policy

Today, the MNE is undertaking an openly procyclical policy. There has been such a significant decrease in budget expenditures that the increase in financing for the Nurly Jol program has nearly completely been absorbed.

In a speech regarding this program, President Nazarbayev said, “I have decided to allocate an additional $3 billion from the National Fund every year from 2015 to 2017. I have instructed the Government to prepare the necessary plans for allocating funds from the National Fund in a week’s time and to consider the necessary funds for this project in the 2015 national budget.”

As was already mentioned, budgetary expenditures in the 2015 budget dropped to 404 billion tenge despite the additional 423.4 billion in financing from the budget. This means that there was actually almost no increase in government spending. These conversations regarding additional anti-crisis funding from the Government simply do not correspond with reality.

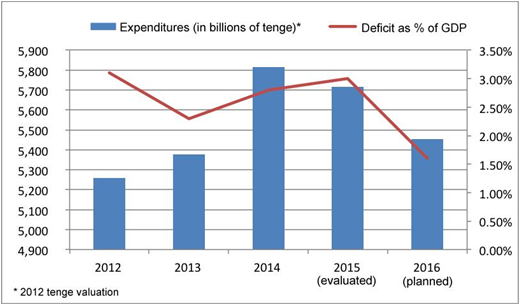

The situation surrounding the 2016 budget is already worse. The figure below shows budgetary expenditures and deficits from 2012 to 2016.

Figure 1. Kazakhstani state expenses and budget deficits, 2012 – 2016

Judging from this data, it is apparent that there has been a significant and systematic decrease in budgetary expenditures.[1] Expenditures have nearly dropped to their 2013 levels, and even the additional financing poured into the Nurly Jol program in 2015 did not lead to a marked increase in comparison with 2014.

The fact that the planned budget deficit has been lowered to 1.6% gives cause for serious concern. As was stressed earlier, there are opportunities for borrowing, i.e. the policy of reducing government spending is targeted and procyclical and will further exacerbate the crisis.

Conclusion

The MNE is not really functioning in its responsibility for in economic planning and the coordination of economic development efforts.

- Planning processes are largely nonexistent. Plans are constantly modified to match the facts ex post facto.

- Due to the constant process of changing projections to match the facts, there is an illusion of effective planning. Realistically assessing the quality of work is difficult, because the overall picture is hidden behind the veil of various adjustments.

- The ineffectiveness of planning was masked by economic growth, but this ineffectiveness began to seriously worsen economic conditions as the crisis deepened between 2013 and 2015.

- While a counter-cyclical economic policy has formally been announced, economic policy has actually been incredibly procyclical for two years and plans for 2016 indicate that this trend will continue.

- All these factors combined reinforce and enhance the economic crisis, making it much worse than it should or could be.

I believe it is patently obvious that the system for budget planning and economic forecasts in Kazakhstan are quite ineffective. This leads to significant problems for the larger economy. The actions of a key economic actor are unpredictable in terms of its spending and financial obligations.

Financial institutions determine budget revenues, and the lack of stability in revenue planning is reflected in fiscal pressure.

Fear of not hitting the mark with regards to the tax plan during a crisis-prone year like 2016 has, on one hand, forced a downward revision of the plan. On the other hand, it has also provoked a level of fiscal pressure on businesses, leading to almost one trillion tenge being pulled out of the economy in the form of unscheduled taxation. This increase in tax revenue levied from businesses exceeds all state support and additional funding programs, which undermines any anti-crisis measures or attempts to inject liquidity to stimulate economic activity.

To solve these problems, it is necessary to enact legislation aimed at limiting the possibility to introduce budgetary revisions during the fiscal year. There are instruments to quickly reallocate funds by means of budgetary reclassification. In the event of a budget shortfall there are instruments in place to reallocate funds from state pensions and the National Fund and there are also significant reserves in external holdings.

If there are restrictions on opportunities for changing the basic parameters of the budget, then the responsibility of the agency in charge of planning will grow, and the state procurement and tax projections processes will stabilize.

[1] Based on the tenge valuation in 2012.

Author: Aidarkhan Kussainov, financial analyst and general director of the Almagest Almagest Management and Strategy Consulting Company (Almaty, Kazakhstan)

The position of the author does not necessarily reflect the position of the cabar.asia editorial board.