“Indeed, in the course of further political disengagement from the West and in the process of Eurasian integration, it is quite natural to expect the recovery of domestic investment and credit quality of the ruble and the tenge, and eventually of the common currency in the EEU”, said Petr Svoik, an economist, PhD (Almaty, Kazakhstan), in an article written for cabar.asia.

The theme of import substitution, which has become fashionable in Russia, emerged recently and suddenly – as a consequence of anti-Russian sanctions and the responsive Russian embargo. Meanwhile, Kazakhstan has become concerned about correcting its raw material export orientation of the economy much earlier and more thoroughly, having achieved notable successes on this way. In any case, such a complimentary understanding of the reforms held in Kazakhstan has been voiced by prominent politicians and economists in Russia, including by those highly critical of “liberals” from the Central Bank and the Government, serving as a reproach and a warning to the latter.

Actually, we would not expect any different Russia’s view of economic policies held in Kazakhstan, just like, however, any specific statistical calculations and illustrations of success of the policy of diversification of the economy and import substitution carried out in Kazakhstan. Well, perhaps, it is unnecessary for Moscow; it is enough just to refer to the telling example of a neighbor, useful for arguing between the “Westerners” and “statists” within the Garden Ring Road.

Meanwhile, the real state of affairs with FIID – forced industrial-innovative development – which has indeed reached the rank of a major economic and political objective of the government of Kazakhstan during recent years, provides food not for praise, but for serious reflection: Why it doesn’t work?

And the key assertion to all that we are going to say below – “does not work” – is based not on our well-known opposition, but on strategic policy documents of the government dedicated to the very industrial development.

Statistics is making happy, reality is depressing

So, the target indicators by 2015: increasing the share of manufacturing industry in GDP to the level of not less than 12.5%; the share of non-raw materials exports – to at least 40% of total exports. These were taken from the purpose of the State Program of FIID for 2009-2014, section “Dynamics of the main socio-economic indicators”[i].

In fact, the share of the manufacturing sector in GDP declined from 11.8% in 2008 to 10.7% in 2013. The share of non-oil products in the country’s exports declined during six years from 28% to 23%. And this statement was taken from the Program “Nurly Zhol” approved by the President (April 2015).

By the way, a strange reference to 2013, while the results of the first five-year plan of FIID was supposed to sum up on 2014, becomes doubly strange against the background of long ago published statistical reports for the past year. Namely, in 2014, the share of manufacturing industry in GDP immediately jumped from 10.7% to 15.44%, exceeding the relevant target indicator of FIID.

The reason why the manufacturing industry suddenly so sharply increased its share in the gross national product in the final year of the industrial-innovative five-year period is a very interesting question, the answer to which explains a lot of things happening now, including, by the way, the early presidential re-election, held seemingly “out of the blue.”

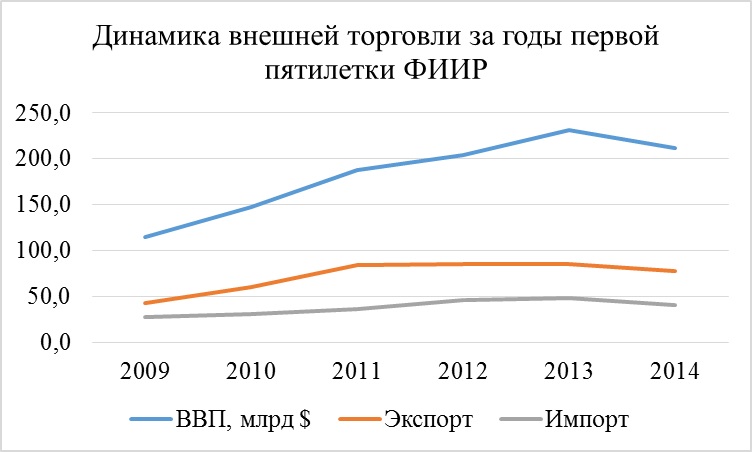

Here’s a chart-tip [i]:

First of all, note that GDP last year dropped sharply, more specifically – from $ 231.875 billion in 2013 to $ 212.25 billion in 2014. This is the official data of the Agency for Statistics. Thus, the drop is 8.46%. The fact is very unpleasant, especially for the liberal market model, anxiously reacting even to a zero growth – recession. Of course, in the next line “in the percentage of the previous year”, the Agency put prosperous 104.3%, but that’s if you count in tenge, which, as you know, was “unexpectedly” devalued by about 19% at the beginning of the final year of FIID.

We will not argue that it was made to get nice statistical indicators. Of course, on the contrary, the devaluation was an attempt to urgently correct the external balance of payments of Kazakhstan that began to “sink” in 2013. Of course, this greatly helped primary goods exporters and brought all national currency reporting into positive dynamics, but the result of such a radical monetary ” exhilaration” is alarming: foreign economic activity in Kazakhstan began to decline.

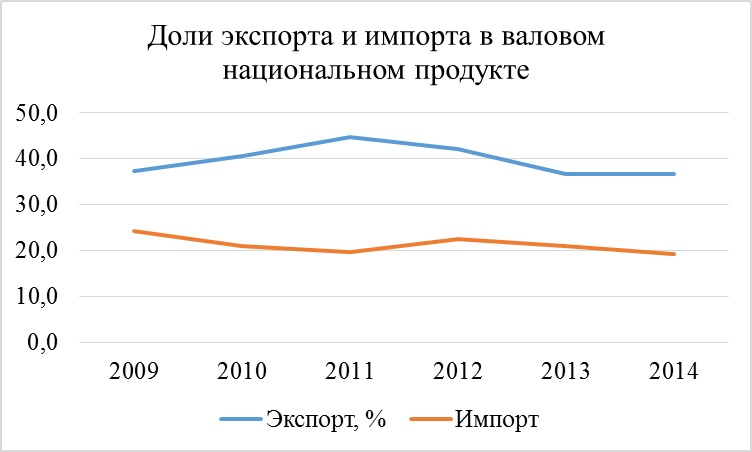

Therefore, the share of non-oil sector in the falling GDP has “skyrocketed”. But what is much more important than the formal statements is that the general dependence of the Kazakhstani economy from excessively high rates of export and import was not reduced by any “enchanting” efforts. Let’s reproduce the same chart in this way:

Source http://www.stat.gov.kz

Exports, as we see, comes up to 40 per cent or more of GDP, and taking into account the transport, energy and construction, the supply of raw materials abroad forms up to three-quarters of the national product. That is, Kazakhstan produces mainly what the country itself does not consume.

The import for consumption in GDP has a share of 20 to 25 percent, and taking into account the transport, trade and construction, the delivery of ready made industrial and consumer goods from abroad is shaping up to half of the national product. That is, Kazakhstan consumes most of what its economy does not produce.

So, a decrease in the share of imports can be traced only during the first three years of the State program of FIID. Although, apparently, the crucial role here is played not by the rising solvency of the population after the crisis of 2007-2008 and the domestic economy consuming imported components, and not by actually growing import substitution in FIID. In any case, the imports to Kazakhstan in recent years is going down together with the decline of exports and the general deterioration of the external economic environment, and not because of industrial progress.

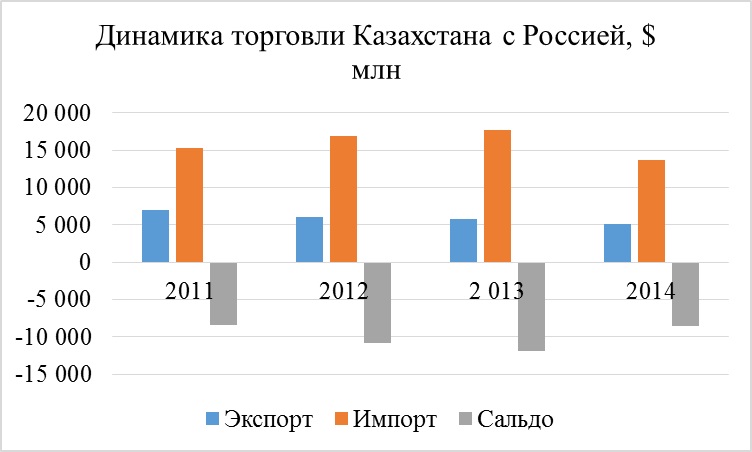

The same statement – that the indicators of dependence on imports reduce not due to the increased domestic productive capacity of the Kazakh economy, but only due to the general deterioration of external economic conditions – also applies to relations between Kazakhstan and Russia:

Source: http://www.stat.gov.kz

One side benefit

The dynamics here covers the period from the beginning of the formation of the Customs Union and gives much food for thought and conclusions. Let’s start with the fact that the stated objective of the CU is the creation of conditions for growth of trade turnover between the member-states, however, one could see that the customs integration is rather working in the opposite direction. For example, exports from Kazakhstan to Russia has been steadily declining with every year, while the growth of Russian imports to Kazakhstan, observed during the first three years, increased only one-sided benefit – the benefit for Russia.

Another paradoxical circumstance here is that Russia, with which Kazakhstan is already a partner in the Eurasian Union, is the most … unprofitable trading partner. This is because Russia does not need Kazakh raw materials. Russia buys some materials only because of still surviving ties that remained from the Soviet Union. More specifically, Russia buys gas condensate from the Karachaganak field for processing at the Orsk plant, the oil from the pipeline “Atyrau-Samara” as a compensation of the supply of oil from Omsk to Pavlodar refinery plant and Ekibastuz coal is for Troitskaya Regional Power Plant and for several other Russian power plants. The rest is a trifle. While Russia itself that is heavily dependent on imports from the EU, the US and even China, remains a manufacturing metropolis for Kazakhstan – a supplier of a large mass of food and other finished goods.

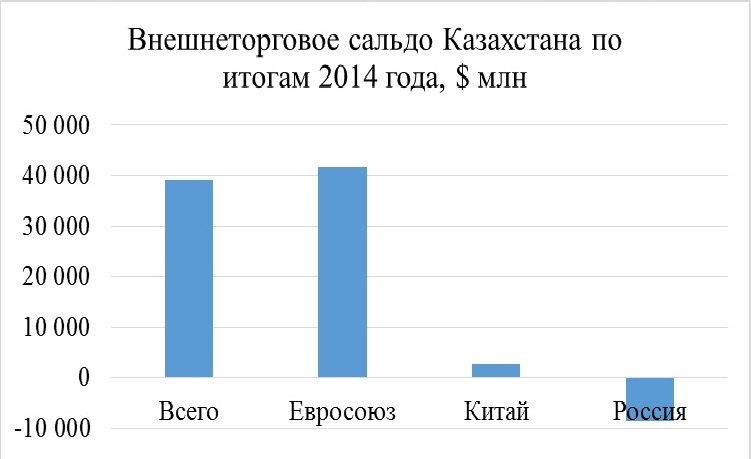

To illustrate this, we give the following eloquent chart:

As you can see, if the largest trade surplus, saving for the Kazakh economy from the standpoint of maintaining the stability of the budget and the rate of tenge, is supported mainly by the trade with the European Union and to a smaller extent – with China, the cooperation with Russia causes dramatic and non-restorable currency costs.

Returning to the previous chart, note that the increasing negative balance in trade with Russia decreased markedly last year, but only because we have tracked the general sharp deterioration in the external economic indicators of Kazakhstan’s economy in 2014. Specifically for Russia, a minus balance became less, because the trade with Russia – both in exports and imports – has «lost ground».

Since the current situation in 2015 and the foreseeable future promises further worsening of external economic difficulties, which Nursultan Nazarbayev truthfully stressed in support of his decision on early elections, let’s try to give an answer, why FIID does not work, and what we must do.

Kazakhstan’s economy: losing the team

After all, popular explanations of unsuccessful industrialization – the corruption and incompetence of the government – did not reflect the full essence. It is not about of the lack of impact of those really big administrative effort and huge financial resources being invested in FIID, but about the opposite result. It is like rowing upstream, which eventually blows away not only a lazy and clumsy team, but also the actually rowing team.

Our answer to what stream brings Kazakhstan’s economy down the export-raw materials channel is as follows: it is foreign investment and foreign funding inside the Kazakh credit process illustrated in the diagram below:

It shows only the most investment-intensive areas of foreign investment. If we tried to put columns on agriculture or, say, food and light industry, they would simply merge to zero axis. The key priorities are obvious: it is not even the raw materials exports, but more geological exploration and engineering research, as well as transport, including pipelines, and construction which is to a large extent directed to the same export of oil and raw materials. In addition, there is trade mostly based on the import of foreign manufactured goods. Finally, it is money: banks and other financial and insurance institutions, fundable from abroad.

And here is an oppositely symmetrical pattern of lending:

Here, we can see that export of raw materials is an outsider, at the same time, an overwhelming advantage is given to all those types of loans that are objectively directed to finance the imports to Kazakhstan of finished industrial and consumer goods. First of all, these are consumer loans that have long and firmly constituted a half or more of the national loan process – mortgages, car loans, loans for the purchase of household appliances, and even for weddings and feasts. Trade and construction are on the second and third places in terms of received loans, and this to a large extent is based on imports, just like, incidentally, residential mortgages.

The question is why the export of raw materials, a key area of Kazakhstan’s economy, has such a modest place in the loan support? How can Kazakh people engaged in raw materials business do without loans of Kazakhstani banks?

The answer to this question reveals the nature of the “controversy” which, despite all the efforts of the government, “blows” Kazakhstan’s economy from industrialization to the dependence on external raw materials export and import of commodity.

The nature of Kazakhstan’s banking system

In the classical industrial economies of the Western type, monetary support of the investment and credit processes is implemented through the national banking system of two levels. The main bank in such a system implements the primary loan issue for banks of the second level, which then distribute it throughout the economy. However, in Kazakhstan (as in Russia), within the framework of the policy of “macroeconomic stabilization”, carried out in the second half of the 1990s, and then “full convertibility of the national currency”, a fundamentally different scheme was introduced, namely: a complete rejection of the national loan issuance and the transition to the issue of its own currency of exchange nature. In this scheme, the National Bank of Kazakhstan does not provide second-tier banks with long-term loan resources at all, supporting them, as appropriate, only by very short-term loans. The National Bank itself acts as a “closing player” on the foreign exchange market, buying foreign exchange surplus of the external balance of payments, or, conversely, selling the lacking currency from its own resources.

In fact, the National Bank acts as only a “national currency exchanger” in such a scheme. The national currency, emitted in the economy only in the form of a projection of the external balance of payments, functions in an objective quality as a “local dollar.”

What is important: all such “exchange” issue of the national currency comes not to second-tier banks, as in a classical scheme, but to raw material exporters, who provide for themselves all the necessary working capital in the country, as well as investments in the expansion of commodity exports, by converting any necessary volumes of foreign exchange earnings into Tenge. In cases where the scale of investment does not allow “pulling” them from the current earnings, “foreign direct investors” begin to act, as we have seen.

In any case, the exporters of raw materials, by virtue of the scheme we described, do not really need a national loan system, and they need Kazakh banks only because current accounts are held there, through which investment operations are carried out.

Accordingly, the second-tier banks, without the basic funding from the National Bank, build the loan process on the deposit basis, while borrowing the required “extra” money from abroad, what actually makes them the banks of the third and lower level – distributors of foreign loans, resold within Kazakhstan.

Of course, the cost of such “loans of the third level” is double and triple. Thus, according to the National Bank, the average rate of tenge loans in March 2015 for legal entities for a period up to one year was 14.6%, more than five years – 11%. For individuals, respectively, it was 21.0% and 13.3%. It is obvious that there aren’t primary manufacturing industries with sufficient profitability to repayment loans of such value in Kazakhstan. “Recapturing” such expensive things can only be possible at speculative trading turnovers and at the land and construction market, where the price bubble is also overblown.

And, of course, citizens in need of shelter and money take mortgage and other consumer loans, despite their cost. They have no other choice, anyway.

The picture of the loan allocation is formed like that. This picture has virtually no pillars of raw materials export economy, but it has the consumer lending based on import.

Conclusions:

Having such foreign investment massively aimed at expanding and strengthening the raw materials export, and having such national loan services massively aimed at expanding and strengthening the commodity import, is it possible to ensure loans and investment to the opposite process, aimed at industrialization, increasing the raw materials processing and import substitution?

The answer is no, of course. The entire experience of the implementation of FIID, in fact, confirms it. Are foreign investors involved in the financing of industrial-innovative development objects? No, the funding is provided mainly by public funds.

How are the public funds allocated for the FIID mainly spent? They are either spent to finance construction works, that is for surrogate replacement of too expensive commercial loans, or to subsidize loan interest, that is to maintain the external credit funding scheme, which is washing out the country’s resources.

Hence, the overall final conclusion is as follows:

The problem of import substitution, which suddenly became acute after the actual start of the “war of sanctions”, has no economic solutions, because the economic system, developed in Russia and Kazakhstan since the end of the 1990s and up to the Maidan and the Crimea issue, was based on a completely different consensus of Western and local political elites. The consensus was – “export of raw materials in exchange for imports of goods, and investment and loans are external”. In fact, the agreement between the monetary and industrial mother country and its financial and commodity provinces managed by comprador oligarchies involved in foreign interests.

The quarrel against the background of the war in Ukraine between Moscow and Washington and Brussels has a well-defined political character, but its economic character remains vague. Partners are fighting against each other in the information and diplomatic field, remaining in an indissoluble, monetary investment credit and commercial export of raw materials partnership.

In such a single monetary organism, the idea of some kind of peripheral national industrialization and import substitution, which goes in the opposite direction from the outer interest of the mother country, is naive and unworkable. However, the sanctions and the confrontation, coupled with a growing global crisis, are pushing for its implementation. Indeed, in the course of further political disengagement from the West and in the process of Eurasian integration, it is quite natural to expect the recovery of domestic investment and loan quality of the ruble and the tenge, and eventually of a common EEU currency.

However, this is just one of the possible future options. We just tried to describe the current state of the fashionable and uncomfortable word “import substitution”.

Petr Svoik – Economist, Ph.D.

The views of the author do not necessarily represent those of CABAR

[i] The article used data from the website of the Agency for Statistics under the Ministry of National Economy http://www.stat.gov.kz

[I] The author of charts is Petr Svoik. The article used the data from the website of the Agency for Statistics under the Ministry of National Economy http://www.stat.gov.kz